Homeowners Insurance in Washington State: What Every Buyer and Seller Should Know Before Closing

Why Insurance Should Be on Every Buyer's and Seller's Radar

Homeowners insurance in Washington State real estate is one of the most overlooked hurdles in a transaction, and also one of the most consequential. Whether you're buying or selling, your ability to obtain affordable coverage can make or break a deal.

This guide covers what both parties need to understand, including personal insurance history, a property's claims record, CLUE reports, and the increasingly common NWMLS Form 22VV.

It's Not Just About the House. It's Also About You.

Insurance Underwriting Looks at More Than the Property

Most buyers assume that qualifying for homeowners insurance depends entirely on the property's condition. In reality, however, that's only half the picture. Insurers also evaluate the buyer's personal insurance history when deciding whether to offer coverage. They use that history to determine the premium as well. This means your past as a homeowner or renter matters more than many people realize.

Your Personal Insurance History Follows You

If you've held homeowners or renters insurance in the past, that history is on file. Insurance companies report claims to a shared database. When you apply for a new policy, carriers pull that record to assess your risk. A history of multiple claims can result in higher premiums or limited coverage options. In some cases, it can lead to outright denial of a new policy. This is true even if those claims were on a previous home or rental property.

The Hidden Risk of Simply Calling Your Insurer

Here's the part that surprises many people. Even calling your insurance carrier to ask about a potential claim can sometimes be noted in your file. That inquiry can then be factored into your future risk profile. Some carriers log these calls as indicators of intent to claim, even if you ultimately decide not to file. As a result, the conversation itself may have consequences down the road. Before you pick up the phone, it's worth understanding that risk.

What You Should Do Instead

The practical takeaway is to be thoughtful and strategic about how you interact with your insurance company. If you're planning to buy a home soon, consider consulting with an independent insurance broker first. They can help you understand how your current record could affect your ability to get coverage on your next property. Another advantage of working with an independent insurance broker is any future calls to inquire about a claim won’t be counted as intent to file.

The Property Has a History Too

Every Home Carries an Insurance Track Record

Just as your personal insurance record follows you, every property carries its own insurance history. Past claims related to water damage, fire, mold, foundation issues, theft, or storm damage are all recorded and can affect a new buyer's ability to insure that property.

Why a Property's Claims History Matters

A home with multiple water damage claims, for example, may be flagged as high risk, leading to higher premiums or coverage exclusions. In some cases, certain insurers may decline to write a policy on the home altogether. This situation isn't just a minor inconvenience. If a buyer can't obtain homeowners insurance, they typically can't close on the home, since lenders require it as a condition of the mortgage. That's precisely why understanding a property's insurance history before making an offer is so important.

What Is a CLUE Report?

Understanding the Database Behind Your Coverage

A Comprehensive Loss Underwriting Exchange (CLUE) report is a detailed record of insurance claims tied to a specific person or property over the past seven years. These reports are generated and maintained by LexisNexis, a consumer reporting agency that collects claims information submitted by insurance companies. Carriers rely on CLUE reports when underwriting and rating new policies, making them a critical piece of the homeowners insurance puzzle in Washington State real estate transactions.

What a CLUE Report Includes

A CLUE report typically includes the following information:

- The homeowner's name, personal details, and policy number

- The date and type of each loss

- The amount the insurance company paid for each claim

- General information about the insurance provider

There are two types of CLUE reports relevant to real estate. A personal CLUE report is tied to an individual's insurance history, while a property CLUE report is tied to a specific home's claims history. Both can play an important role in a real estate transaction.

How to Get a CLUE Report

Under the Fair Credit Reporting Act, homeowners are entitled to one free CLUE report every 12 months. You can request your report through LexisNexis by visiting consumer.risk.lexisnexis.com or by calling 1-866-312-8076. Reports are typically delivered within 15 days of the request.

Advice for Home Buyers: What to Do Before You Make an Offer

Check Your Own CLUE Report First

Before you start house hunting seriously, request your personal CLUE report from LexisNexis. Reviewing it gives you a chance to correct any errors and set realistic expectations about your coverage options going forward.

Ask the Seller for the Property's CLUE Report

This is a critical step that many buyers overlook as sellers have not been providing this in the past. Buyers and real estate agents cannot independently pull a CLUE report on a property they don't own. Only the homeowner can request it. However, you can ask the seller to provide a copy. A property CLUE report shows any claims filed in the last seven years, giving you a much clearer picture of the home's risk profile and what you might face when shopping for homeowners insurance in Washington State.

Keep in mind, it can take several weeks for a property’s CLUE report to be delivered to the seller. If you make your offer conditional on reviewing a CLUE report, it could hold up the transaction and/or make your offer less competitive. I expect to see sellers providing CLEAR reports more in the future, much like a Seller-Provided Inspection, but it is not widespread at this time.

Don't Assume a Clean Report Means No Issues

A blank CLUE report could mean the home had no problems. Alternatively, it could mean the owner handled repairs out of pocket and never filed a claim. It might also mean their insurer simply doesn't report to LexisNexis. Regardless of what the CLUE report shows, a professional home inspection remains essential and should never be skipped.

Review Any Claims Carefully

If the report does show past claims, don't panic right away. A single claim for a repaired roof isn't necessarily a red flag. On the other hand, multiple water damage claims or repeated claims for the same issue warrant serious scrutiny. Large payouts for mold or foundation problems are also cause for concern. In those situations, consult with an insurance broker before you proceed.

Advice for Sellers: Get Ahead of the Issue

Request Your CLUE Report Before You List

As the homeowner, only you can pull the property's CLUE report, since buyers are not able to do it themselves. Being proactive by obtaining the report before you list builds trust with buyers and helps keep the transaction on track. Having it ready to share demonstrates transparency and can remove a major source of anxiety from the process.

One important caveat: CLUE reports can take up to 15 days to receive. Don't wait until you're under contract to request it. The time to pull your report is before you list, not after an offer comes in. Providing it upfront can make the sale go more smoothly and reassure buyers from the start. This policy is not widespread among home sellers at this time but expect it to become more of a concern in the future.

Review the Report for Errors

CLUE reports occasionally contain inaccurate information. Those errors can unfairly harm your sale. If you find mistakes, you have the right to dispute them with LexisNexis. Common errors include claims attributed to your property that you didn't make, incorrect dollar amounts, or outdated entries. Correcting errors in advance protects buyers from making decisions based on faulty data.

Be Prepared to Explain Past Claims

A claims history doesn't have to be a dealbreaker. If you can show that issues were properly resolved, buyers are often reassured. For example, if the report shows a water damage claim from five years ago, be ready to share documentation of the repair work. Context matters both to buyers and to their insurance carriers.

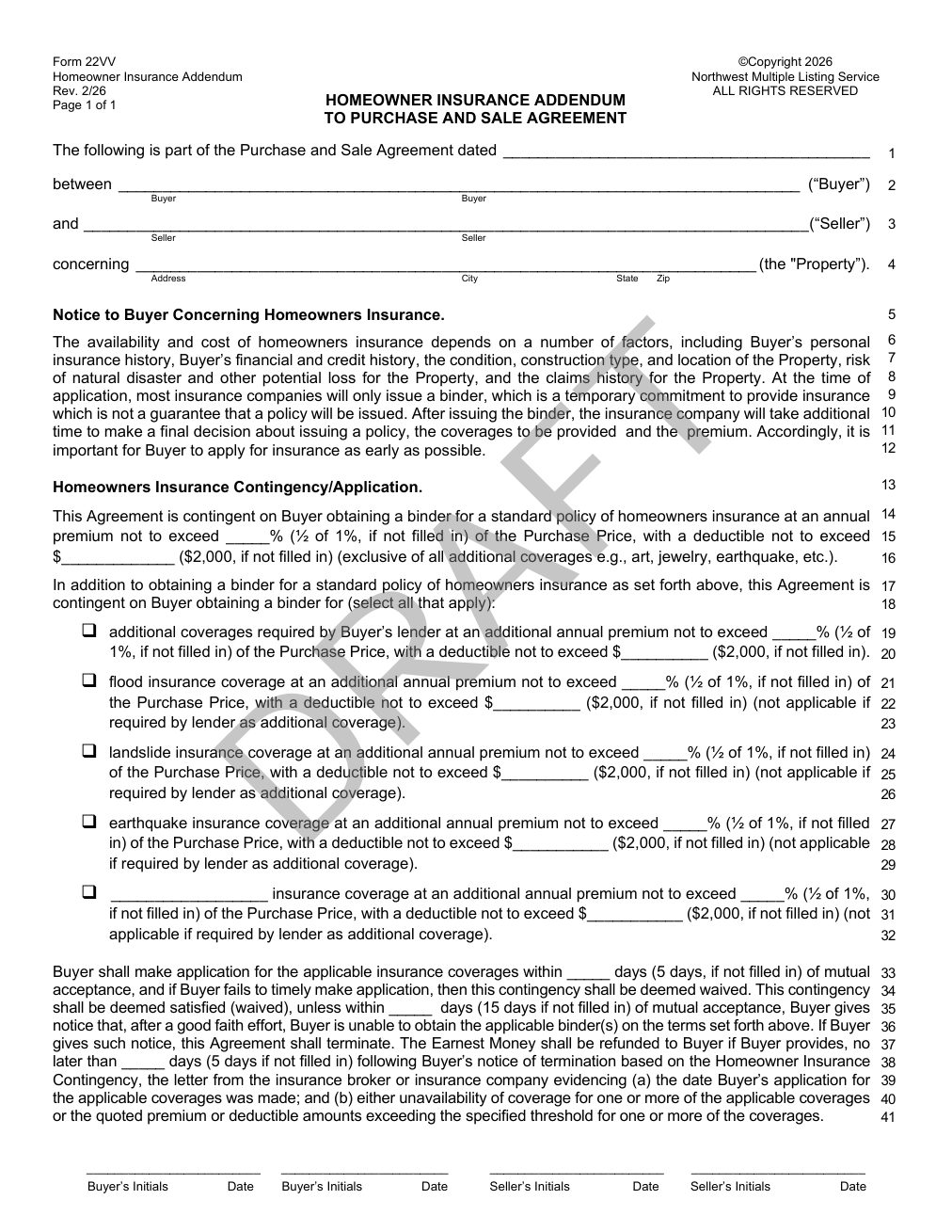

The NWMLS Form 22VV: What Washington State Buyers and Sellers Need to Know

What This Addendum Is and Why It Matters

In Washington State, the NWMLS Form 22VV, also known as the Homeowner's Insurance Addendum, is becoming increasingly common. It acknowledges that obtaining homeowners insurance is an important condition of the sale. Furthermore, it gives the buyer a formal mechanism to address insurance-related concerns before closing.

For Buyers: How Form 22VV Protects You

The 22VV addendum generally gives buyers the right to investigate the property's insurability during the transaction. It also provides a basis for terminating the purchase and sale agreement if acceptable coverage cannot be obtained on reasonable terms. Specifically, a buyer may be able to back out of the contract under the following circumstances:

- They are unable to obtain homeowners insurance at all due to the property's claims history or condition

- The only available coverage comes at a premium that is unreasonably high compared to similar homes

- They are unable to obtain: flood, landslide, earthquake, etc coverage at or below a premium/deductible amount agreed upon in advance by the buyer and seller

If this addendum is included in an offer, it creates a meaningful contingency that could impact a buyer’s ability to close on a sale. Sellers absolutely need to take it seriously.

For Sellers: Read This Addendum Carefully

If you receive an offer that includes Form 22VV, pay close attention to its terms. This addendum gives the buyer real leverage to walk away from the deal. They can do so if they encounter insurance obstacles that are outside your control as a seller. For instance, a home with a complicated claims history may trigger unexpected insurance concerns. The same is true for homes with deferred maintenance or certain structural characteristics.

Compare to Your Own CLUE Report

As a seller, the best way to protect yourself is to be proactive. Pull your CLUE report early, address any known property conditions that could raise red flags for insurers, and make repair documentation available. Work with your agent to anticipate potential insurance objections before they surface mid-transaction.

Pay Attention to the Requested Terms

Before accepting an offer with a 22VV, review the requested terms carefully. A good place to start is comparing the terms to your own insurance coverage to gauge whether they feel reasonable. Also review your CLUE report to see whether any items listed may impact the buyer’s application for coverage.

Talk to an Insurance Broker if Necessary

Lastly, talk to an insurance broker to see if they feel the buyer's insurance terms are reasonable or whether they may impact the buyer’s ability to close. Your real estate agent should have a good contact that can help support this portion of the offer review.

Key Takeaways

For Buyers

Your personal insurance history matters, not just the property's. Request your CLUE report before you start shopping. Ask sellers for the property CLUE report early in the process. Be cautious about how you interact with your current insurer, because even routine inquiries can be logged and counted against you. Additionally, if Form 22VV is part of your offer, make sure you understand how it protects you and what your options are if insurance becomes a problem.

For Sellers

Only you can pull your property's CLUE report, so don't leave that to chance or wait too long. Request it before you list, since it can take up to 15 days to arrive. Review it carefully for errors and be prepared to provide context for any past claims. If Form 22VV appears in an offer, treat it as a serious contingency and prepare accordingly well before you're under contract.

The Bottom Line

Homeowners insurance in Washington State real estate has always been a factor in transactions. In today's market, however, it is increasingly a make-or-break issue. Underwriting is tighter, premiums are rising, and both buyers and properties face more scrutiny than ever. Getting ahead of it is no longer optional.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.