Homeowners Insurance in Washington State: What Every Buyer and Seller Should Know Before Closing

Why Insurance Should Be on Every Buyer's and Seller's Radar

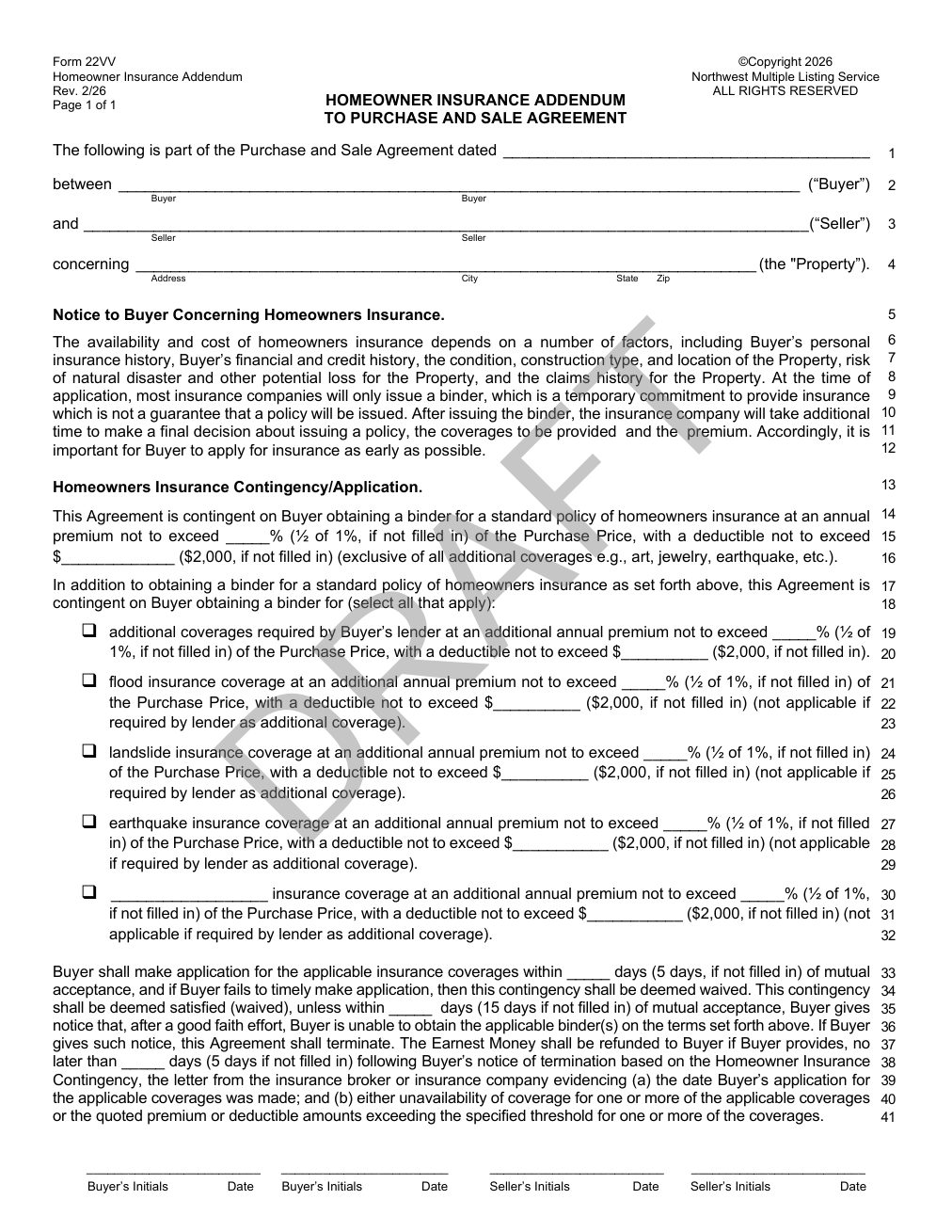

Homeowners insurance in Washington State real estate is one of the most overlooked hurdles in a transaction, and also one of the most consequential. Whether you're buying or selling, your ability to obtain affordable coverage can make or break a deal.

This guide covers what both parties need to understand, including personal insurance history, a property's claims record, CLUE reports, and the increasingly common NWMLS Form 22VV.

It's Not Just About the House. It's Also About You.

Insurance Underwriting Looks at More Than the Property

Most buyers assume that qualifying for homeowners insurance depends entirely on the property's condition. In reality, however, that's only half the picture. Insurers also evaluate the buyer's personal insurance history when deciding whether to offer coverage. They use that history to determine the premium as well. This means your past as a homeowner or renter matters more than many people realize.

Your Personal Insurance History Follows You

If you've held homeowners or renters insurance in the past, that history is on file. Insurance companies report claims to a shared database. When you apply for a new policy, carriers pull that record to assess your risk. A history of multiple claims can result in higher premiums or limited coverage options. In some cases, it can lead to outright denial of a new policy. This is true even if those claims were on a previous home or rental property.

The Hidden Risk of Simply Calling Your Insurer

Here's the part that surprises many people. Even calling your insurance carrier to ask about a potential claim can sometimes be noted in your file. That inquiry can then be factored into your future risk profile. Some carriers log these calls as indicators of intent to claim, even if you ultimately decide not to file. As a result, the conversation itself may have consequences down the road. Before you pick up the phone, it's worth understanding that risk.

What You Should Do Instead

The practical takeaway is to be thoughtful and strategic about how you interact with your insurance company. If you're planning to buy a home soon, consider consulting with an independent insurance broker first. They can help you understand how your current record could affect your ability to get coverage on your next property. Another advantage of working with an independent insurance broker is any future calls to inquire about a claim won’t be counted as intent to file.

The Property Has a History Too

Every Home Carries an Insurance Track Record

Just as your personal insurance record follows you, every property carries its own insurance history. Past claims related to water damage, fire, mold, foundation issues, theft, or storm damage are all recorded and can affect a new buyer's ability to insure that property.

Why a Property's Claims History Matters

A home with multiple water damage claims, for example, may be flagged as high risk, leading to higher premiums or coverage exclusions. In some cases, certain insurers may decline to write a policy on the home altogether. This situation isn't just a minor inconvenience. If a buyer can't obtain homeowners insurance, they typically can't close on the home, since lenders require it as a condition of the mortgage. That's precisely why understanding a property's insurance history before making an offer is so important.

What Is a CLUE Report?

Understanding the Database Behind Your Coverage

A Comprehensive Loss Underwriting Exchange (CLUE) report is a detailed record of insurance claims tied to a specific person or property over the past seven years. These reports are generated and maintained by LexisNexis, a consumer reporting agency that collects claims information submitted by insurance companies. Carriers rely on CLUE reports when underwriting and rating new policies, making them a critical piece of the homeowners insurance puzzle in Washington State real estate transactions.

What a CLUE Report Includes

A CLUE report typically includes the following information:

- The homeowner's name, personal details, and policy number

- The date and type of each loss

- The amount the insurance company paid for each claim

- General information about the insurance provider

There are two types of CLUE reports relevant to real estate. A personal CLUE report is tied to an individual's insurance history, while a property CLUE report is tied to a specific home's claims history. Both can play an important role in a real estate transaction.

How to Get a CLUE Report

Under the Fair Credit Reporting Act, homeowners are entitled to one free CLUE report every 12 months. You can request your report through LexisNexis by visiting consumer.risk.lexisnexis.com or by calling 1-866-312-8076. Reports are typically delivered within 15 days of the request.

Advice for Home Buyers: What to Do Before You Make an Offer

Check Your Own CLUE Report First

Before you start house hunting seriously, request your personal CLUE report from LexisNexis. Reviewing it gives you a chance to correct any errors and set realistic expectations about your coverage options going forward.

Ask the Seller for the Property's CLUE Report

This is a critical step that many buyers overlook as sellers have not been providing this in the past. Buyers and real estate agents cannot independently pull a CLUE report on a property they don't own. Only the homeowner can request it. However, you can ask the seller to provide a copy. A property CLUE report shows any claims filed in the last seven years, giving you a much clearer picture of the home's risk profile and what you might face when shopping for homeowners insurance in Washington State.

Keep in mind, it can take several weeks for a property’s CLUE report to be delivered to the seller. If you make your offer conditional on reviewing a CLUE report, it could hold up the transaction and/or make your offer less competitive. I expect to see sellers providing CLEAR reports more in the future, much like a Seller-Provided Inspection, but it is not widespread at this time.

Don't Assume a Clean Report Means No Issues

A blank CLUE report could mean the home had no problems. Alternatively, it could mean the owner handled repairs out of pocket and never filed a claim. It might also mean their insurer simply doesn't report to LexisNexis. Regardless of what the CLUE report shows, a professional home inspection remains essential and should never be skipped.

Review Any Claims Carefully

If the report does show past claims, don't panic right away. A single claim for a repaired roof isn't necessarily a red flag. On the other hand, multiple water damage claims or repeated claims for the same issue warrant serious scrutiny. Large payouts for mold or foundation problems are also cause for concern. In those situations, consult with an insurance broker before you proceed.

Advice for Sellers: Get Ahead of the Issue

Request Your CLUE Report Before You List

As the homeowner, only you can pull the property's CLUE report, since buyers are not able to do it themselves. Being proactive by obtaining the report before you list builds trust with buyers and helps keep the transaction on track. Having it ready to share demonstrates transparency and can remove a major source of anxiety from the process.

One important caveat: CLUE reports can take up to 15 days to receive. Don't wait until you're under contract to request it. The time to pull your report is before you list, not after an offer comes in. Providing it upfront can make the sale go more smoothly and reassure buyers from the start. This policy is not widespread among home sellers at this time but expect it to become more of a concern in the future.

Review the Report for Errors

CLUE reports occasionally contain inaccurate information. Those errors can unfairly harm your sale. If you find mistakes, you have the right to dispute them with LexisNexis. Common errors include claims attributed to your property that you didn't make, incorrect dollar amounts, or outdated entries. Correcting errors in advance protects buyers from making decisions based on faulty data.

Be Prepared to Explain Past Claims

A claims history doesn't have to be a dealbreaker. If you can show that issues were properly resolved, buyers are often reassured. For example, if the report shows a water damage claim from five years ago, be ready to share documentation of the repair work. Context matters both to buyers and to their insurance carriers.

The NWMLS Form 22VV: What Washington State Buyers and Sellers Need to Know

What This Addendum Is and Why It Matters

In Washington State, the NWMLS Form 22VV, also known as the Homeowner's Insurance Addendum, is becoming increasingly common. It acknowledges that obtaining homeowners insurance is an important condition of the sale. Furthermore, it gives the buyer a formal mechanism to address insurance-related concerns before closing.

For Buyers: How Form 22VV Protects You

The 22VV addendum generally gives buyers the right to investigate the property's insurability during the transaction. It also provides a basis for terminating the purchase and sale agreement if acceptable coverage cannot be obtained on reasonable terms. Specifically, a buyer may be able to back out of the contract under the following circumstances:

- They are unable to obtain homeowners insurance at all due to the property's claims history or condition

- The only available coverage comes at a premium that is unreasonably high compared to similar homes

- They are unable to obtain: flood, landslide, earthquake, etc coverage at or below a premium/deductible amount agreed upon in advance by the buyer and seller

If this addendum is included in an offer, it creates a meaningful contingency that could impact a buyer’s ability to close on a sale. Sellers absolutely need to take it seriously.

For Sellers: Read This Addendum Carefully

If you receive an offer that includes Form 22VV, pay close attention to its terms. This addendum gives the buyer real leverage to walk away from the deal. They can do so if they encounter insurance obstacles that are outside your control as a seller. For instance, a home with a complicated claims history may trigger unexpected insurance concerns. The same is true for homes with deferred maintenance or certain structural characteristics.

Compare to Your Own CLUE Report

As a seller, the best way to protect yourself is to be proactive. Pull your CLUE report early, address any known property conditions that could raise red flags for insurers, and make repair documentation available. Work with your agent to anticipate potential insurance objections before they surface mid-transaction.

Pay Attention to the Requested Terms

Before accepting an offer with a 22VV, review the requested terms carefully. A good place to start is comparing the terms to your own insurance coverage to gauge whether they feel reasonable. Also review your CLUE report to see whether any items listed may impact the buyer’s application for coverage.

Talk to an Insurance Broker if Necessary

Lastly, talk to an insurance broker to see if they feel the buyer's insurance terms are reasonable or whether they may impact the buyer’s ability to close. Your real estate agent should have a good contact that can help support this portion of the offer review.

Key Takeaways

For Buyers

Your personal insurance history matters, not just the property's. Request your CLUE report before you start shopping. Ask sellers for the property CLUE report early in the process. Be cautious about how you interact with your current insurer, because even routine inquiries can be logged and counted against you. Additionally, if Form 22VV is part of your offer, make sure you understand how it protects you and what your options are if insurance becomes a problem.

For Sellers

Only you can pull your property's CLUE report, so don't leave that to chance or wait too long. Request it before you list, since it can take up to 15 days to arrive. Review it carefully for errors and be prepared to provide context for any past claims. If Form 22VV appears in an offer, treat it as a serious contingency and prepare accordingly well before you're under contract.

The Bottom Line

Homeowners insurance in Washington State real estate has always been a factor in transactions. In today's market, however, it is increasingly a make-or-break issue. Underwriting is tighter, premiums are rising, and both buyers and properties face more scrutiny than ever. Getting ahead of it is no longer optional.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

Using Earnest Money Strategically

How to Make Your Earnest Money a Competitive Advantage

By Kayvon Mohammadian ⋅ 02/21/2026

When you're ready to make an offer on a home, earnest money becomes your first opportunity to show commitment. Therefore, using earnest money strategically can make all the difference in a competitive market.

Read below to learn how to make your earnest money a competitive advantage and stand out from the crowd.

What This Article Includes:

1. What is Earnest Money?

2. Can I Lose My Earnest Money?

2. How Much Should You Offer?

3. The Power of More

4. The Non-Refundable Deposit

5. My Recommendation

What is Earnest Money?

Earnest Money is a Deposit

Earnest money is essentially a deposit you make after your offer is accepted. Think of it as a good-faith gesture that demonstrates your commitment to the purchase. Don’t worry, it’s not an added cost on top of the purchase price. It becomes part of your down payment at closing.

Held By Escrow

The buyer provides their earnest money directly to the escrow company, not the seller. Buyers usually deliver it via check or wire within 2 or 3 days after the seller accepts their offer. In most cases, the escrow company holds it until the closing date when they lump it together with the rest of the funds for the seller.

Pro Tip:

Be sure you at least have funds for earnest money readily available when you need them. You don’t want to get stuck waiting for investments to sell or money to transfer to your account. This could cause you to be late with delivering the earnest money and be in breach of contract.

Your Earnest Money Holds You to the Contract

Once a seller accepts your offer, both parties become legally bound to the contract. The seller cannot back out and must proceed with selling their property as agreed. Similarly, you as the buyer are held to the contract with your earnest money at stake if you break the agreed upon terms. Think of it as collateral you provide to ensure you abide by the terms of the contract

Can I Lose My Earnest Money?

Earnest Money Is Protected by Your Contingencies

If the deal falls through due to legitimate reasons covered by your contract’s contingencies, you'll usually get this money back. However, if you simply change your mind without a valid reason, the seller may be entitled to keep it. Conversely, if the seller defaults on the contract, the escrow company protects and returns your earnest money to you (and you may be entitled to further damages from the seller).

Common Contingencies That Protect Earnest Money

An Inspection Contingency is one of the main parts of your offer that can protect your earnest money. If you are conducting an inspection and decide not to purchase the house for any reason, you will receive your earnest money back. However, if you have passed the inspection period you no longer have that protection.

The Financing Contingency is another common contingency that protects you in multiple ways. The first is if your lender rejects your loan through no fault of your own, you can back out of the purchase with your earnest money. It also protects you in case the home does not appraise for the amount you agreed upon.

There are many other parts of your offer that can protect your earnest money. Such as: Title Contingency, HOA Review Period, Neighborhood Reviews, Feasibility Studies, and many others. Make sure you understand these contingencies and how they can protect you. Keep in mind, the more contingencies you utilize in your offer, the less competitive it will make you in a multiple offer scenario.

How Much Should You Offer?

Use Your Earnest Money Strategically

There is no minimum or maximum amount of earnest money required for an offer. Although, if you are only putting down $1000 sellers won’t take you seriously. It should be enough that the seller feels comfortable knowing that you won’t walk away from the deal without cause. Remember, you should use your earnest money strategically to stand out from the crowd.

Offer at least 3%

Typically, we recommend at least 3% of the property’s purchase price. Anything less and a seller may feel that you are not fully committed. You don’t want the seller to move to the next buyer over fears that you may walk away for no reason.

The Median Home price in Seattle in 2026 is around $850,000. In that case, you should plan on offering at least $25,000 as your earnest money. Keep in mind many buyers offer more than that so if you are expecting to compete you should consider offering above 3%.

The Power of More

Going Beyond the Standard

In a competitive situation, consider increasing the amount of your earnest money beyond 3%. It is a way to show that you are fully committed to the sale and will not back out. No buyer wants to lose their earnest money and sellers will feel reassured. You are less likely to walk away from $50,000 than $20,000. However, legally you cannot lose more than 5% of the purchase price if the deal falls through. Of course, losing any amount of earnest money is never the plan regardless of legal protection.

In Multiple Offer Scenarios Sellers Will Notice

Many buyers often wonder how much a seller will care about the amount earnest money. If you are not competing with other buyers, it may not be the biggest factor whether your offer is accepted or not. However, if the seller is comparing multiple offers that are very similar to one another, it is something they will note. Using your earnest money strategically will make a difference.

When we are preparing our clients to compete for a home, we do whatever we can to make our offer stand out. Earnest money is one of the first things a seller will notice on the first page of your offer. This is a chance to show immediately that you are committed. If you are doing whatever you can to stand out, don’t overlook this important factor.

The Non-Refundable Deposit

Aggressive, Risky, and It Works!

Now, let's discuss a more aggressive approach: converting your earnest money into a non-refundable deposit. This is the most impactful way you can use your earnest money strategically. However, I must warn you that this tactic can carry significant risks.

By making all or part of your deposit non-refundable, you're instructing escrow to release that money directly to the seller before closing. Escrow usually turns it over to the seller just a few days after they accept your offer.

I know this sounds crazy but it is an effective way to get your offer noticed and hopefully convince a seller to choose you. You are enticing them with the potential of receiving your earnest money in a few days. This is particularly helpful for sellers who are low on funds and may have additional expenses associated with selling or moving to a new home. Plus, who wouldn’t want to be offered a large check almost immediately rather than 3 to 4 weeks?

Why Buyers Choose This Strategy

Recently, many buyers in hot markets have embraced this approach. This is because most aggressive offers already waive contingencies that protect earnest money. Contingencies like the inspection, financing, and title are the first to be waived when competing. Therefore, few scenarios exist where you'd recover those funds if you decided not to buy the house. That is, of course, unless the seller fails to uphold their end of the contract.

Your Commitment is Clear

By offering a non-refundable deposit, you're simply accelerating the timeline. It shows that you are, without a doubt, committed to purchasing the home. If you have waived all contingencies and you convert your earnest money to a non-refundable deposit, you will obviously do whatever you can to make the sale go through. That has real value to the seller.

Understanding the Risks

When converting your earnest money to a non-refundable deposit, it doesn't mean sellers can simply walk away and keep your money. Both you and the seller must uphold the terms of the contract. Nevertheless, if the seller does try to back out and keep your earnest money, you'll likely need to pursue legal action to recover it.

As for all our recommendations in real estate, don’t do anything that will keep you up at night. If you have doubts about your ability to uphold your end of the contract, then this strategy is not right for you. Talk to your real estate agent to be sure you understand the level of competition and help determine whether this is necessary or not.

My Recommendation

Make You Earnest Money Work For You

Your earnest money is one of the first things a seller will notice about your offer. It is right near the top of your offer on the first page and a chance for you to show your intent. You should plan on offering at least 3% of the purchase price to make it clear you intend to move forward with the sale. Remember, depending on your contingencies you will receive the earnest money back if you decide not to proceed with the purchase.

Consider the Non-Refundable Deposit

If you are expecting to compete for a home, you should seriously consider converting your earnest money into a non-refundable deposit. This strategy is aggressive and not for everyone but it can make the difference between you getting the house or not. There are very real risks associated with it so be sure you understand what you are signing up for.

Understand the Risks and Get the House!

Being sure you understand what you are signing up for holds true for every aspect of a home purchase. We are confident in our approach because, after hundreds of transactions, we have never had a buyer lose their earnest money. It is only after careful consideration and risk assessment that we are able to help our buyers be as competitive as possible, while protecting what is important.

If you would like to know more about utilizing your earnest money to get a house or other parts of the home buying process, reach out anytime.

FRAUD WARNING

Always be cautious when wiring funds. Fraud is rampant in real estate transactions. Be sure to double check any wiring instructions before sending funds. The best practice is to verify wiring instructions by contacting the escrow company from a publicly available phone number.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

Do I Need a Sewer Scope When Buying a Home?

Mike from Sewer Inspector scoping a sewer line

When you're buying a home, it's easy to get caught up in the excitement of finally finding the right one. One thing many buyers find themselves asking is "do I need a sewer scope when buying a home?" My advice is always the same: do not overlook or underestimate a home's sewer line. That's where a sewer inspection comes in. Read more to learn everything you need to know about sewer scopes.

What this Article Includes:

1. What Is a Sewer Scope?

2. What Does the Inspector Look For?

3. Common Sewer Issues

4. Common Repairs Techniques

5. The Importance of Doing A Sewer Scope with Your Home Inspection

6. Negotiating Items from the Sewer Scope

7. Who to Trust

8. The Bottom Line

What Is a Sewer Scope?

Don’t Skip it During Your Home Inspection

A sewer scope is a video inspection of the home's sewer line, which runs from the house to the city's main sewer connection. An inspector uses a camera attached to a flexible cable to record footage of the interior and determine it’s condition. A sewer scope is generally not included in a standard home inspection, so any issues are unlikely to be discovered though that.

We always recommend our buyers get a sewer scope done while doing their due diligence and considering purchasing a home. The scope typically covers the entire length of the line, from the house all the way to where it connects to the main municipal system. This important inspection gives you a comprehensive look at the health of your sewer line so you can flush with peace of mind.

What Does the Inspector Look For?

What You Need to Know

During a sewer scope, the inspector is examining the condition, functionality, and structural integrity of the sewer line. They're checking for any signs of damage, blockages, or deterioration that could lead to backups, leaks, or complete failure.

They'll also assess the type of material the line is made from, the grade or slope of the pipe (to ensure proper drainage), and the quality of the connection to the city main. Essentially, they're looking for anything that could cause problems now or down the road — and in older homes, that list can be surprisingly long.

Common Sewer Issues

Cracks and Breaks

Sewer scopes often reveal a range of issues, some minor and some that require serious attention. Cracks and breaks in the pipe are among the most concerning, as they can allow wastewater to leak into the surrounding soil or let groundwater seep in, leading to backups and contamination. In extreme cases, leaking wastewater can wash away the soil under the line and cause the line to collapse.

Low Spots

Low spots or "bellies" in the line occur when sections of pipe sag, creating areas where waste and debris can collect and cause blockages over time. These low spots are a common occurrence in many sewer lines and not always a cause for concern. If water and debris are continuing to flow though it may require no action. However, you will want to be aware of them and monitor it in case it gets worse and leads to a blockage in the future.

Offsets

Offsets are another common occurrence when sections of pipe become misaligned at the joints, creating a lip where they meet. While a minor offset might not cause immediate problems, even a small one can catch debris and waste as it flows through the line. Over time, offsets can worsen as roots exploit the gap or as continued settling increases the misalignment.

Root Intrusions

Root intrusions are incredibly common around the Seattle area. It is especially likely in older homes with mature trees and large plants nearby. Tree roots are drawn to the moisture in sewer lines and can infiltrate through cracks or joints, eventually clogging or even crushing the pipe.

Deterioration

Deterioration is another frequent finding, particularly in homes built several decades ago. Pipes made from outdated materials like concrete, clay, or cast iron can deteriorate, crack, or collapse over time. Aging concrete sewer lines are a common issue in the Seattle area as they will eventually erode and the bottoms become more prone to breaks and cracks.

Breaks at the City Main

The connection to the city main is the final critical point of inspection. If this connection is faulty, damaged, or improperly installed, it can also lead to recurring backups. These issues are particularly concerning because any repairs will require coordination with the city. Main sewer lines are most often located in the middle of the street and repairing may require breaking open the street to access it. As you can imagine, this can result in the cost to repair growing exponentially so it’s one that we are always very cautious about.

Common Repairs Techniques

If your sewer scope uncovers issues, the good news is that there are several repair options available. A full sewer line replacement is actually quite uncommon and clever repairs can save you lots of money.

Jetting the Line

Jetting the line is one of the most straightforward and cost-effective solutions, especially for blockages caused by debris buildup or minor root intrusions. A high-pressure water jet is used to clear out the pipe, restoring flow and preventing backups. It's a relatively quick process and can extend the life of your sewer line significantly when done as part of regular maintenance.

Spot Repair

For more serious problems like cracks or breaks, a spot repair may be necessary. This involves excavating the area around the affected portion of the pipe, removing the damaged section, and replacing it with new material. While this sounds intensive, it's often localized to just one area rather than the entire line, making it far less costly than a full replacement. In many cases, only a few feet of pipe need to be addressed.

Sewer Lining

Another increasingly popular option is lining the sewer line, also known as trenchless repair or cured-in-place pipe (CIPP) lining. This method involves inserting a flexible, resin-coated liner into the existing pipe. It is then inflated and cured to form a new, seamless pipe within the old one. It's less invasive than traditional excavation, can address multiple issues at once, and often comes with a long warranty. While it's more expensive than jetting or a simple spot repair, it's still significantly cheaper than replacing the entire line.

Proactive Repairs Are Always Cheaper!

The key takeaway here is that proactive repairs, whether it's jetting, spot repairs, or lining, will always be far less costly than waiting until the sewer line fails completely and requires a full replacement. Catching problems early through a sewer scope and addressing them strategically can save you thousands of dollars and a lot of headaches down the road.

The Importance of Doing a Sewer Scope with Your Home Inspection

Sewer Scopes are Not Usually Included in a Home Inspection

Your general home inspection covers a lot of ground — the roof, foundation, electrical, plumbing fixtures, HVAC, and more. But a standard inspection doesn't include looking inside the sewer line. There are many ways that a sewer line can fail and you won’t know without a sewer scope. This separate service is one you absolutely shouldn't skip when deciding on your next home.

Repair Costs Start in the $1000’s – Don’t Get Stuck With Someone Else’s Problems!

Sewer line repairs or replacements can easily cost anywhere from a few thousand dollars to $20,000 or more. It’s largely dependent on the severity of the issue and the accessibility of the line. A shallow sewer line can be dug out by hand and easily repaired if needed.

However, if your sewer line is 4 feet deep or more, it requires more permits and safety measures and will add to the cost of the repair. A quality sewer inspection can also tell you how deep the line is and where exactly and breaks may be located to better help you plan for necessary repairs.

Sewer Scopes Allow You to Plan and Budget for Repairs

By getting a sewer scope done alongside your general inspection, you're getting a complete picture of the home's condition before you finalize the purchase. It's a small upfront cost (usually $250-300) that can save you from a major financial surprise down the road. Plus, if issues are found, you have the opportunity to address them during the negotiation phase.

I tend to think of a sewer scope as very cheap “insurance.” They are usually straightforward as there isn’t much ambiguity about any potential issues. You will also receive a written report with a video of the entire sewer line. With this, you can easily shop around the repairs to different contractors and get the best possible price.

Negotiating Items from the Sewer Scope

What to negotiate?

If your sewer scope reveals problems, you have options. Like any item that may come up on an inspection, your options are:

1. Negotiate with the seller to have the issues repaired before closing

2. Ask for a credit toward the cost of repairs

3. Adjust the purchase price to account for the work that needs to be done.

Be Very Specific With Your Negotiations

If you negotiate to have the seller repair the item before closing, be sure you are very specific about how you would like it done. As previously mentioned, you and your agent should send the sewer inspection to multiple sewer contractors. Be sure to their recommendations and bids for the repair so that you can include it in your negotiations. That allows you to choose the best course of option and specify exactly how you want the seller to repair it and which company to choose.

Be Prepared to Walk Away

In some cases, you may elect to walk away entirely if the sewer issues are extensive and the seller isn't willing to address them. The key is that the sewer scope gives you leverage and information. This information is invaluable during negotiations. Without it, you could be on the hook for expensive repairs just weeks or months after moving in, with no recourse. A sewer scope puts you in control, allowing you to make an informed decision and protect your investment.

Who to Trust?

Choose an Independent Sewer Inspector

When planning for a sewer scope for my clients, whether buyers or sellers, we always go with an independent sewer inspector. My favorite inspectors specialize in inspections and nothing else. This benefits you because they have no incentive to misrepresent the condition of a sewer line.

A company that does inspections as well as repairs may overstate the issues in hopes that you will hire them to conduct costly repairs. With a company that only does inspections, they mostly cater to people planning to buy or sell a property. They will know exactly what matters to you and how to move forward in the most cost effective way. Remember, you can take your inspection and use it to get repair bids from other companies if needed.

The Bottom Line

A sewer scope might not be the most exciting part of buying a home, but it's one of the smartest moves you can make. It uncovers hidden problems that could cost you tens of thousands of dollars, gives you negotiating power, and provides peace of mind that you're not inheriting someone else's sewer nightmare. When you're already investing in a home inspection, adding a sewer scope is a no-brainer.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

PLANNING FOR PRE-INSPECTIONS

By Kayvon Mohammadian ⋅ 01/31/2026

How to Plan for Pre-Inspection in a Competitive Market

One of the very first items that people think about when purchasing a home is the inspection. This is your chance to learn everything you can about its condition, defects, and deferred maintenance so you know what you’re getting yourself into. Planning for potential pre-inspections is an important first step in finding the right house for you.

Before our local housing market became so competitive, the norm was to have this done after the seller accepts your offer. However, now things move much quicker and buyers must do more to get a seller to accept their offer. Waiving their inspection contingency is a common tactic that immediately makes a buyer’s offer more attractive, but it is not without risk.

Read below to learn more about planning for pre-inspections and how to navigate the process safely and competitively.

Included In This Article:

1. Why Waiving the Inspection Contingency Strengthens Your Offer

2. Understanding Seller-Provided Inspections

3. Understanding Buyer Pre-Inspections

4. Budgeting for Multiple Pre-Inspections

5. The Bottom Line

Why Waiving the Inspection Contingency Strengthens Your Offer

When Competing for a Home, It's a Must Do

In competitive markets, waiving the inspection contingency often makes the difference between winning and losing a home. Sellers will always prefer offers without this contingency because it removes a major opportunity for the deal to fall apart.

During a traditional inspection period, buyers can renegotiate the price, request repairs, or back out entirely. If a buyer backs out with their inspection contingency they would be entitled to have their earnest money returned. Consequently, sellers view inspection contingencies as risky.

Buy "As Is" With Confidence

When you waive inspection, you're telling the seller you'll buy the home "as-is" at the agreed price. It can also speed up the closing period which sellers often value. In multiple-offer scenarios, this certainty often outweighs even higher-priced offers with contingencies.

While I frequently recommend that buyers waive the inspection contingency, it is only after reviewing a pre-inspection. Either by doing one themselves or relying on one provided by the seller. This ensures you know exactly what you're buying.

Understanding Seller Provided Pre-Inspections

A Good Seller Provided Pre-Inspection Helps Everybody

In today's competitive market, many sellers order their own inspections before listing their home. This benefits everyone involved as sellers can address issues upfront or price accordingly. Meanwhile, buyers can review the inspection without spending money on their own.

When a seller provides an inspection, they're showing transparency about the property's condition. Sellers are required by law to provide any home inspection they have and disclose any condition issues that may have been discovered.

Additionally, it saves every interested buyer from paying for their own inspection on a house that they may not get. With a seller provided inspection, multiple buyers can review the same report and make informed decisions.

Review With Caution

However, you should approach seller-provided inspections with caution. Not all inspection companies maintain the same standards. You and your agent should carefully review the report for thoroughness. If the report seems too clean or lacks detail, consider it a red flag. In that case, conduct your own pre-inspection with a trusted inspector.

Once you're satisfied with the seller's inspection, you can confidently waive your inspection contingency. This makes your offer more competitive while protecting yourself. You've already done your due diligence which means you can move forward knowing the home's true condition.

Understanding Buyer Pre-Inspections

A pre-inspection is when the buyer hires an inspector to evaluate a home before submitting an offer. You may decide to do a pre-inspection because the house you are targeting is going to be competitive and the seller has not provided an inspection. Or if the seller is providing an inspection but you don’t fully trust it or want to verify with your own inspection.

It's Cheap Insurance When Finding The Right Home

Pre-inspections give you a significant advantage in multiple-offer scenarios, especially if the seller is not providing one. You'll know exactly what repairs or issues exist before committing, which will help inform the rest of your offer. Also, if the inspection reveals major problems, you simply move on to the next property.

No one wants to pay for an inspection of a house that they do not end up buying but think of it as relatively cheap insurance. The lost cost of an inspection is better than buying a house that requires expensive repairs that you were not aware of.

Budgeting for Multiple Pre-Inspections

Plan For at Least a Couple

Now, let's talk about realistic budgeting. In today's market, I tell my buyers to plan to do at least a couple pre-inspections and sewer scopes. That means about $800-$1000 per house. These days, you will pay around $600 for the inspection and $275 for the sewer scope. So, you should set aside $2,000-$3000 for any potential pre-inspections you may need.

Of course, planning to spend thousands of dollars on inspections for homes you don’t ultimately buy feels like wasted money. We try to avoid this whenever possible, but it must be factored into the cost of buying a home.

Think of it like this, the median home price for a single family home in Seattle for 2025 was about $800,000. A few thousands of dollars to find the right home without a laundry list of repairs needed will be worth it in the long run.

In our current market, most sellers are providing their own inspections. So you hopefully won’t have to spend your own money on unneeded inspections but it’s good practice to be aware of this when you start your home search.

The Bottom Line When Planning for Pre-Inspections

Utilize Pre-Inspections and Get the House!

In a competitive housing market, expect to be required to waive the inspection contingency when competing for a home. This may require a cost to you upfront if the seller is not providing an inspection or you do not trust it. However, they save you from making costly mistakes. They also give you confidence to compete effectively. In a market where waiving inspection is often necessary, knowing the true condition matters. You need that information before you commit.

If you're starting your home search, I'm here to help. I can guide you through inspections and competitive offers so you find the right house. Reach out anytime to discuss your situation.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

How to Choose the Right Buyer's Agent

Choosing the buyer's agent is the most important first step towards finding your next property. It means the difference between a smooth, successful home purchase and a frustrating one filled with missed opportunities. After years of working with buyers in Seattle's competitive market, I've learned what separates exceptional agents from the rest.

Here's my tips on how to find the right real estate agent that you should look for when selecting someone to represent you.

Start with Trusted Referrals for Buyer's Agents

Talk to People You Trust

The best agents build their business on referrals, not just advertising. Start by talking to friends, family, and colleagues who have recently bought or sold homes in your target area. Ask them about their experience: Did their agent communicate well? Were they responsive? Did they fight for the best deal?

Personal recommendations are far more valuable than any online review alone. Insights from people you know and trust who've seen the agent in action will help you make an informed decision. Plus, agents are likely to provide their best service to referrals who come from a previous client. They want that person to keep recommending them so more good word of mouth is always a positive for agents and buyers.

Evaluate the Brokerage, Not Just the Agent

Culture Matters

A key tip when looking for the right real estate agent, is not to overlook the brokerage they work for. A company's culture directly influences how their agents present themselves and advocate for their clients. In today's competitive market, you don't want a discount brokerage that cuts corners on service and support.

Find a Brokerage With a Large Market Share

Instead, look for a company with significant market share in the neighborhoods where you're searching. Why does this matter? Because agents at these established firms are constantly talking with each other about what they're seeing in the market.

At Windermere, we share insights about pricing trends, buyer activity, and inventory changes that happen daily or even hourly. When the market moves fast, having an agent plugged into this network gives you a crucial information advantage.

Speed Matters: Why You Need an Agent Who Can Move Fast

The Best Ability is Availability

In today's competitive real estate market, timing is everything. Homes can go under contract in a matter of days or even hours. This means you need a buyer's agent who can get you through the door quickly. The last thing you want is to miss out on your dream home because your agent couldn't make time for a showing until next week.

That's why working with a part-time agent or someone with limited availability can be a real disadvantage. Real estate doesn't operate on a 9-to-5 schedule, and neither should your agent. You need someone who's responsive, flexible, and ready to drop everything when a new listing hits the market or when you want to see a property before it's gone.

Find a Team You Trust

One of the best ways to ensure you always have access when you need it is to work with an agent who's part of a team. A well-coordinated team means there's always someone available to show you a home, answer your questions, or write up an offer at short notice. It's the kind of backup and support that can make all the difference when competition is fierce and every minute counts.

This is why working with a buyer's agent like myself who has the support of working with a team makes such a big difference. You can be confident that there is always a ready, willing, and able agent available to support you whenever the time arises. By getting two agents at the same time there is double the strategizing and support. Sometimes we don't always agree on the best course of action so you also get multiple perspectives. Real Estate is not a "one size fits all" practice so the more data and insight you get allows you to make informed decisions at every step.

Look for Agents Who Go Beyond the MLS

Find a Proactive Buyer's Agent

Here's a question that separates good agents from great ones: "What do you do to research listings I'm interested in beyond just looking at the MLS?"

The answer should involve proactive outreach to listing agents. I make it a point to call the listing agent for every property my clients are considering and stay connected with them. You'd be amazed at what you can learn from a simple phone conversation that you'd never find online.

I've had listing agents share detailed information about competing offers already on the table (something I would never do for my own listings, but it has certainly helped my buyers). Others have told me that the seller would be open to reducing the price, they are looking for a specific concession, or that another buyer is preparing to submit an offer so we need to move quickly. All of this intelligence helps my clients craft stronger, more strategic offers.

Find a Connected Buyer's Agent

A good buyer's agent can also tap professional networks beyond fellow brokers. It helps to stay in contact with photographers, stagers, title company, contractors, and anyone else who may have insights that we do not. Are photographers and stagers booked up? Is the title company getting an uptick in requests for Preliminary Title Report? That can mean there is soon to be an increase in inventory that you should be aware of. It may mean the difference between settling for an "okay" house or confidently waiting for the right one coming soon.

Constant Communication Makes the Difference

Your Agent Should Know What's Happening

When my clients are targeting a property, I stay in constant contact with the listing agent. I'm gathering real-time updates on activity, interest level, last minute pre-inspections, and many other important details. This ongoing dialogue is crucial before and after an offer is accepted so you can keep adjusting as needed. It is the most impactful factor that informs our strategy and allows us to write the strongest offer possible.

Remember, until the seller has formally accepted an offer, you can always adjust yours as needed. Buyers working with a proactive agent will always have an advantage when it comes to getting their offer accepted. A few last minute tweaks of your offer can often push you just ahead of the competition when it really matters.

The Bottom Line

It's More Than Just Key's and Paperwork

The right agent doesn't just unlock doors and fill out paperwork. They leverage their network, actively research on your behalf, and use every tool at their disposal to give you an edge in competitive situations. When you're making one of the biggest financial decisions of your life, you deserve an agent who goes the extra mile.

Reach Out to See How Kayvon and Cara Can Help You

If you're looking for a dedicated team of advocates who knows the Seattle market inside and out, I'd love to talk about how I can help you achieve your real estate goals. Feel free to reach out at any time. I'm always happy to answer questions, even if you're just starting to explore your options.

Finding the right real estate agent is just one of the steps towards the home buying process.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

How to Find the Right Lender

You found the perfect house, made a strong offer, and then lost out to another buyer. What went wrong? Sometimes the difference isn't your offer price or earnest money, it's your lender.

In competitive markets, sellers don't just evaluate your financial qualifications. They also consider whether your lender has the experience, responsiveness, and local market knowledge to close the deal smoothly. Choosing the right mortgage lender can be the deciding factor between getting your dream home or watching it go to someone else.

Continue reading to learn how to find the right lender and turn your financing into a competitive advantage.

What This Article Includes:

1. It's More than Just and Interest Rate

2. Communication is Key

3. Where to Find the Right Mortgage Lender

4. The Takeaway

It's More than Just an Interest Rate

Choosing the Right Lender Matters

Knowing how to find the right lender is more than just a low interest rate. Of course, that is the most important thing for you, but there is more to consider in a competitive market. You will likely come across a multiple-offer situation in any hot housing market with low inventory and high demand. Make sure your lender is not holding you back.

Sellers Will Take Lenders into Account

Since sellers have multiple buyers to choose from, listing agents look at many different factors that go into a buyer's financing beyond their down payment amount. They want to be sure that a buyer's lender is experienced and familiar with the fast-paced housing market. That is why you need a lender who understands the challenges that buyers face and can help you stand out.

Communication is Key

One Point of Contact

When you are trying to find the right lender, you should have one point of contact handling your loan. Both you and your agent must have their cell phone number and email so you can reach them directly. Ideally, there will be an open flow of communication with text and email chains keeping everyone up to date.

Keep Everyone Up To Date

It is helpful for your lender and agent to know the state of your loan, what properties you are going to be pursuing, and what tactics you will be employing. When looking to buy a competitive property, things can and often do happen fast and you may need to reach out to your lender at all hours of the day. The best lenders understand that this is a normal aspect of their job and will take the time to support a buyer when they need it.

Let Your Lender be Your Advocate

These factors make the difference for buyers getting the house they want so keep it in mind when choosing your lender. That is why communication between your lender and listing agents is also important when making a competitive offer. When you go to submit your offer, make sure your lender is calling the listing agent on your behalf. This is a chance for the lender to tell the listing agent about your qualifications and answer questions. This is something that your agent should facilitate but it is a worthwhile question to ask of your lender. You can use this when interviewing lenders to gauge their familiarity with common practices when working in our housing market.

Where to Find the Right Mortgage Lender

Start With a Recommendation From Your Agent

Now that you know how to pick the right mortgage lender you can start looking for the ones that fit your criteria. Start by talking with your real estate agent. They should have a list of recommended lenders who they have worked with in the past and who have a proven track record of success.

Make Sure You Choose a Reputable Lender

In general, I recommend avoiding big banks, online lenders, and credit unions. They have a bad reputation as being hard to contact and practices that can make them less competitive in a multiple-offer situation. Your experiences may vary but just be sure they know the area you are targeting and that they understand how the local market works. You can also ask friends, family, or coworkers who have bought a home recently who they used and what their experiences were.

Get Three Quotes!

Remember that you are looking for a mortgage lender who can combine a good working relationship as well as provide a good interest rate. I recommend at least talking to three lenders in your area to find the best fit. If you find one lender you like but another has a better rate, try asking the first one if they can meet or beat the other rate. It is a normal part of the process and can save you lots of money over the life of your loan. Finding the right mortgage lender can take time and effort but using the right one can mean the difference between getting your dream home or not.

The Takeaway

Three Main Points: Communication, Reputation, and Rates

Choosing the right mortgage lender involves more than just securing a low interest rate. In competitive markets, your lender can make or break your offer. Sellers and listing agents evaluate not only your financing terms but also your lender's reputation, responsiveness, and market knowledge. Therefore, working with an experienced local lender who understands fast-paced markets gives you a significant advantage.

Communication is critical when selecting a lender. You need a single point of contact who responds quickly via phone, text, and email at all hours. Moreover, your lender should proactively advocate for you by calling listing agents to discuss your qualifications and answer questions. This personal touch can set your offer apart in multiple-offer scenarios.

Recommendations

Start by asking your real estate agent for lender recommendations based on their successful past transactions. Generally, avoid big banks, online lenders, and credit unions, as they often lack the local market expertise and accessibility needed in competitive situations. Instead, interview at least three local lenders to compare both rates and working relationships. Don't hesitate to ask your preferred lender to match a competitor's rate—it's standard practice. Ultimately, the right lender combines excellent communication, competitive rates, and the ability to help you win your dream home.

About the Author | Kayvon Mohammadian

As a local Seattlite born and raised in West Seattle, Kayvon brings a deep love for the area and a passion for helping people navigate one of life's biggest decisions. After graduating from Bishop Blanchet High School in 2010 and Washington State University in 2014, Kayvon joined Windermere Real Estate in 2017. There he learned the craft from his mother, Cara Mohammadian, and her decades of experience in the industry. Now they work together as a team to provide the highest possible level of service for their clients. That foundation has given him not only the technical knowledge of the business, but also the relational skills it takes to truly serve clients during what can be one of the most emotionally and financially charged experiences of their lives.

Today, Kayvon combines the art and science of real estate to guide his clients through the complexities of buying and selling a home. Whether it's identifying a property with strong bones and timeless craftsmanship or recognizing those that fall short, Kayvon brings a keen eye for style and quality that goes beyond the listing sheet. He stays current on local market trends and statistics to ensure his clients are making informed, confident decisions not just with their hearts, but with their heads. With hundreds of clients served, his goal is to be a trusted guide and help each new client come out on top. Whether they're buying their first home or selling their next one.

When he's not helping clients, Kayvon is enjoying life in West Seattle with his wife (Maddie), two kids (Soraya and Kian), and dog (Philip J Fry). You can usually find him on Alki struggling to contain his two kids in a wagon as his dog pulls him along the beach or at home working on his house.

NEW BUYER AGENCY AGREEMENT IN 2024

Starting in 2024, there are major changes to agency and broker services between Real Estate Agents and their clients. Buyers will no longer be able to meet with an agent and tour homes casually without a signed buyer agency agreement. Everyone is now required to sign an agency agreement for a broker to provide real estate services.

This legislation is the first of its kind in the country and will increase transparency for buyers and prevent ambiguity. This change is an adjustment for both the consumer and Real Estate professionals alike. You need to know what to expect for you to be an informed consumer in this ever-changing housing marketplace.

CHANGES TO THE LAW

Most people around Seattle have likely never signed a buyer agency agreement when working with an agent. While home sellers have always had to sign a similar agreement, no such requirement existed for buyers. The home-buying process relied on a casual approach intended to give buyers more freedom.

Few agents wanted their buyers to sign contracts because The Law of Real Estate Agency already applied. It stated that any broker who performed “real estate brokerage services” had formed an agency relationship with that client already. In doing so, the standard agency duties would have already been applied to protect the buyer. Also, the agent could rightfully represent the buyer and be provided with compensation for their work.

Now, the changes are intended to make the agent’s compensation clear to the buyer from the beginning. The new agency agreement specifies the rate of compensation an agent will work for and how they will receive compensation. Much like how a contractor will provide a list of services and the cost, so will real estate agents through the agency agreement.

WHY THE REQUIREMENT FOR A BUYER AGENCY AGREEMENT?

The law surrounding broker agency agreements remained largely unchanged for 25 years. The last major change came in 1998 and allowed agents to represent buyers in real estate transactions. Before that, buyer’s agents were considered to work for the seller which put brokers and buyers in a precarious position. With that arrangement, it left no one explicitly working for the buyer’s best interests. That is why they initiated changes outlining that brokers owed their buyers specific fiduciary duties to protect home buyers.

While the buyer agency was improved in 1998, buyer’s agents continued to receive compensation paid out of the seller proceeds. For that reason, the impression could be that they did not cost the buyer anything, which isn’t correct. The cost of the buyer’s agent is included in the purchase price and should be considered to have been paid by both parties. Although in many cases that was never made explicitly clear.

These most recent changes are part of a concerted effort by Washington State and the NWMLS to improve transparency for the consumer. Other recent changes allowed sellers to list homes on the NWMLS that did not offer a buyer’s agent compensation. It also made the compensation public so that buyers could see the rate at which their agent would be paid.

WHAT YOU NEED TO KNOW ABOUT THE BUYER AGENCY AGREEMENTS

This change requiring a Buyer Agency Agreement is certain to create some confusion and misgivings among brokers and their clients. However, the goal is to help home buyers become more aware consumers and avoid any implication the seller pays compensation. Knowing these key points will make you a more informed and proactive buyer in this ever-changing housing market.

TERM LENGTH

The default term that any buyer agency agreement lasts is 60 days. Of course, the buyer and broker have the option to extend that term length at the initial signing or after it expires. Many brokers may want to extend that from the beginning. As anyone who purchased a home in a competitive market knows, it can take months to find the right house. If you trust your broker, it would be prudent to go ahead and extend that agreement beyond 60 days from the beginning.

EXCLUSIVE OR NON-EXCLUSIVE

EXCLUSIVE BUYER AGENCY AGREEMENT

Buyers will have to specify whether the agreement gives that agent the exclusive or non-exclusive right to represent them. An exclusive agency agreement means that only that agent may represent that buyer in purchases. For brokers, such agreements give them certainty that the work they do will lead to payment in the future. Of course, that only happens if the buyer finds a property they want to buy.

An exclusive agency agreement would also put more pressure on the broker to provide the best possible service. Brokers will know if they don’t live up to their client’s expectations, they will simply cancel their agreement and find someone who will.

As a potential home buyer, you should be aware that the agent you signed an exclusive agency with is owed compensation when you purchase a property. That stands even if you use another broker to purchase that property. If the exclusive agency is still active, that broker could attempt to claim the compensation.

No broker wants to go through the effort and bad appearance of suing a former client to get paid, but this new legislation opens the possibility. Be sure to cancel any exclusive agency agreement you may have signed if you decide to work with a different broker.

NON-EXCLUSIVE BUYER AGENCY AGREEMENT

Many buyers may feel more comfortable with a non-exclusive agreement. That would allow them to sign similar agreements with multiple brokers, should they feel the need to do so.

For those who are looking for properties across a large geographic area, a non-exclusive agreement could be a good option. That would allow multiple agents to help you in locations that the others may not cover. Your agency agreement may also specify geographic areas that it covers and could allow exclusive rights for just that area.

Regardless of the location, many brokers will not want their clients working with other agents within their area. This agreement will help buyers and their representatives clarify ahead of time what the relationship will cover and provide certainty for both parties.

COMPENSATION

The clarification of buyer broker compensation is the most notable change to buyer agency in Washington State. It clarifies the amount that a broker is to be paid as soon as they begin offering buyer services. In doing so, it also allows buyers to negotiate that compensation ahead of time.

With this change, buyers could request that any amount of compensation above a certain threshold be credited to themselves. At the same time, brokers could set a minimum rate at which they agree to be paid at closing. It also allows brokers to negotiate with a seller if they are not providing compensation or it does not meet their minimum.

Currently, buyers are not able to pay their agent’s compensation as part of their home loan. By allowing brokers to negotiate with sellers for their pay, they can avoid putting an extra financial burden on the buyer.

CANCEL YOUR BUYER AGENCY AGREEMENT ANYTIME

If you are a home buyer, you may feel uncertain about signing a contract with a broker early on. Keep in mind that the law states that the Buyer Agency Agreement: “must be entered into before, or as soon as reasonably practical after, a broker begins rendering real estate brokerage services to the buyer.” (RCW 18.86.120).

The consensus among real estate professionals is that this requirement will left up to interpretation, at least initially. What exactly qualifies as “rending real estate brokerage services” is not clearly defined. Many agents will insist on signing one early on to avoid inadvertently breaking the law. At the same time, others will not feel comfortable forcing clients to sign a contract early on and may wait. There will certainly be some discrepancies in how different brokers handle it, especially in the early period of these new requirements.

Fortunately, home buyers working with us at Windermere only need to provide written notice to terminate the buyer agency agreement. As long as you have not had an offer accepted, you can unilaterally cancel your agreement with no recourse. The goal of this change is to ensure that the control remains in the hands of the consumer. Brokers do not want to force anyone into a working relationship they are unhappy with.

MORE TRANSPARENCY IS A GOOD THING

These updates to buyer agency agreements are the biggest change in how we buy and sell homes in a quarter of a century. Through increased transparency and buyer education, buyers can ensure they have the level of control they want over their home purchases. It will require adjustments for brokers and their clients, but the result is a more informed and happier homeowner. Be sure to do your part as an informed consumer and